HI6026 Audit, Assurance and Compliance Assessment Answer

Answer

Audit, Assurance and Compliance

Week 1

Assurance engagement

Assurance engagement refers to the practice of engagement exercised by practitioners to enable the company to understand and make opinions about the subject matter’s measurement. The opinions generated by the engagement practice induces the level of confidence in the user. There are two types of assurance that are provided by the professionals namely, limited assurance and responsible assurance. Responsible assurance takes the party into consideration who will provide all required information and data to the practitioners so that they can provide assurance to the user company. The information providing company is therefore, the responsible party (Knechel and Salterio, 2016). The objective behind exercising engagement assurance is to assure the users on the responsible party for the information and details which are presented to them.

Mainly three varied tasks are performed by the OEL’s audit manager. The financial analysis of the Local Pty Ltd will be undertaken to provide trustworthy assurance to the user company.

| Tasks | Types of level of assurance |

| The management accounts for the year ended 30 June 2017 | The CEO of the company OEL feels that the requirement to check the financial status of the company before 2016 is not required. However, she emphasizes on auditing the management accounts for the year ended 30 June, 2017. Therefore, auditors will be required to follow up the procedures that OEL agreed upon. |

| All transactions occurring from the date negotiations commenced until the settlement date | The OEL company’s CEO is not concerned about the transactions that happened before the negotiation date. However, the auditor requires the information of all the transactions happened to clarify from their responsibility. But the CEO only wants assurance to be provided of the transactions that occurred between the negotiation date to the final date of settlement. |

| Local’s financial report prepared at the acquisition date | To provide a high level of the confidence, the auditors are needed to perform an intense audit of the financial statements to reduce any chances of faults. The audit reports will assist the OEL company to make opinions regarding the value enhancement in the Local after its acquisition. |

Week 2

Liabilities and responsibilities of the Auditors

There are numerous responsibilities that an auditor has to provide to entrust the confidence of the users. The auditor has to derive reliable conclusions from the company’s financial reports. Along with the conclusions the auditor is also responsible for collecting reliable evidences to prove the drawn conclusions. However, even after such intensive research, the auditor is not expected to provide 100% assurance over the matter. Moreover, it is a risky way to depend completely on the predicted outcomes from the reports. Even though a 100% assurance cannot be provided, the auditors perform their function without any chance of faulting. This is because there are set standards of performing audits and the auditors has to follow them to avoid future complexities (Gimbar, Hansen and Ozlanski, 2016).

In the case of Data Ltd, the company was sanctioned a loan by Better Bank ltd on the basis of the data they received from the company. The company’s financial statements assured the bank that the loans will be repaid. But the Data Ltd came across difficulties in business therefore, now the company lack funds to pay back the loan. In this situation, the Data Ltd cannot hold the auditors accountable for this. The auditor only has access to the information that is made provided to him. He cannot provide audit statements beyond the provided data. Therefore, it is not the responsibility of the auditor to identify the faults and frauds of the company. He is only responsible for auditing the provided data. The Data Ltd company is therefore, solely responsible for their inability to payoff loans.

Week 3

Independence of auditor

The responsibility of the auditor is to perform auditing of the given reports by being independent of the unhealthy ways that can be used (Tepalagul and Lin, 2015). For example, biased towards the company. These factors should never be incorporated by the auditor while examining the reports and he should be aware of the limits of dependency and independency that the audit standards provide (Maroun, 2017). There are various threats to the independency that an auditor faces and some of them are explained below in the context of Hall & Associates:

- Self interest threat is defined by the APES 110 where, due to personal interest, the company may fall prey to the risks. The CGL company’s board has indicted to pay the fees of Hall & Associates in CGL shares. The auditing company therefore, may also receive some financial benefits due increase in the share values. The gain of financial interest is therefore, a self-generated threat by the company. however, there are ways in which the self interest threats can be safeguarded:

- Proper consultation and suggestions from professionals can protect the auditors from self interest threat.

- An effective action plan against the consequences of the threat can assist the auditors.

- If the problems do not solve, the auditor can also vacate his position.

- Intimidation threat is imposed by the CGL company on the auditing firm. This is identified because the company intimidates Hall & Associates to not disclose the asset ratio by saying that 0.9:1 is a temporary asset ratio and the company is financially sound. The company also indicated that it will rethink in engaging the auditors in other functions if they choose to disclose the actual asset ratio. The audit firms can use the following safeguards against the intimidation threat:

- Consultation and suggestions from experienced professionals.

- Audit team should include experienced members.

- If require, reorganize the engagement terms.

- Self-review threat is another threat that the auditing company faces. This is because, the Hall & Associates is engaged in providing the efficiency of the internal controls. It was involved in redesigning the software and now it is assigned to perform audit including the IT department of the company. in such cases the auditors can act bias towards their own work. Therefore, the threat of self-review can arise. The ways in which this threat can be avoided are:

- Involve independent auditors in the team who are not working in the same firm.

- Individual auditor should consider working properly and bias free as their responsibility.

- If problems persist, then auditor can vacate the position.

Week 4

Types of audit associated risks

There are three potential risks in audit functions. They can arise if the auditor is involved in providing irrelevant assurance to the company. The risks are (Abdullatif and Kawuq, 2015):

- Inherent risks: these risks are not under company’s control and material statements made in reports are the results of these risks.

- Control risks: these risks arise when internal control of the system is ineffective in detecting the errors in the statements.

- Detection risk: these risks are the result of ineffective functioning and performance of the auditor in identifying and correcting the misstatements in the reports.

In the current situation, the following risks of Sampson Limited are confirmed:

- The responsibility of handling the funds of the organization is fulfilled by the treasurer. The company’s financial controller is earning profits in the terms of foreign currency for the Sampson Limited. These foreign transactions are found to showcase inherent limitations (Samsonova and Humphrey, 2015). Therefore, the risk that exist in this case is inherent risk Control risk can also arise due to the factors like authorization towards funds.

- The financial controller of the company failed to provide appropriate provision because he could not determine the redeployment of the assets and this can give rise to inherent risk.

- A controlling system is required because the company has decided to provide bonus base on the sales of individual employee. If the controlling system face some technical issues then it might fail. Therefore, control risk is also displayed in this scenario.

- The probability of the controlling issues in the closing and opening balances can give rise to inherent risk. moreover, specialized trainings would be required for new software. This can result in control risks.

- Detection and control risk may rise because there is no provision for checking the functions of the controlling system. In such cases, the problems go unnoticed therefore, even auditors cannot detect the issues in the reports.

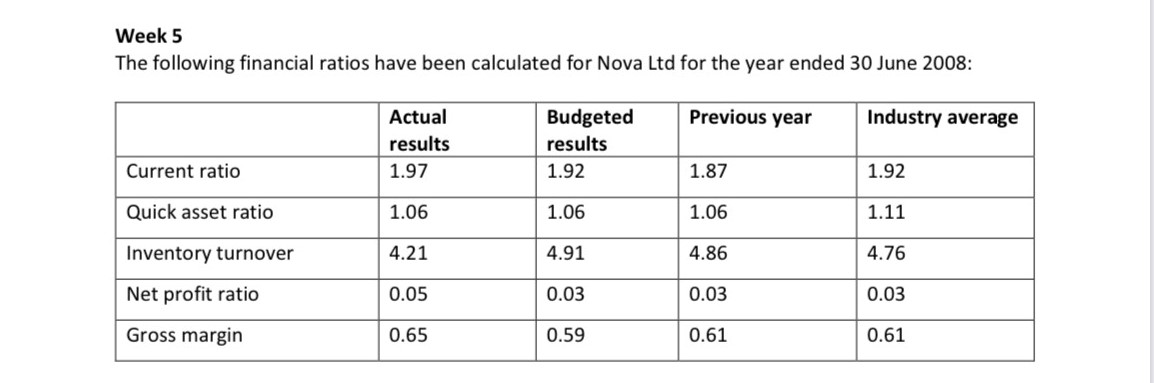

Week 5

Ratios

Ratios provide assistance in comprehending the firm’s financial results. The ratios also allows the firms to compare and analyze its performance (Arkan, 2016). The ratio analysis of the company Nova Limited are shown below in the table:

| Ratios | Description |

| Current | Nova Limited’s current ratio shows the ability of the company to payoff short-term loans and debts. |

| Inventory turnover | This ratio displays that in the present year, inventories are replaced 4.21 times by Nova Limited. This shows that the market has demand for company’s products. |

| Net profit | Income through different sources has allowed company to make profit 0.05 times. |

| Gross margin | The company was able to make profit 0.65 times from the currently operating functions. |

| Quick asset | the company can payoff short-term debts without needing prior realization of inventories. |

Customer Testimonials